Retirement Planning for Small Business Owners: Tax-Smart Strategies to Build Wealth & Reduce Stress

For many small business owners, retirement planning falls to the bottom of the priority list. Between managing expenses, supporting clients, and keeping operations running, long-term financial planning can feel like a luxury—something “regular employees” get to worry about.

But here’s the truth: retirement planning isn’t just for employees.

It’s one of the most powerful wealth-building tools available to small business owners—and one of the most overlooked.

A well-structured retirement plan not only prepares you for the future but also reduces your tax burden today. The earlier you start, the more control you gain over your money, your business, and your peace of mind.

Let’s break down exactly how to build a retirement strategy that supports your life and your business.

Intro: Why Retirement Planning Isn’t Just for Employees

As a small business owner, you are the employer, the employee, and the CFO of your future. Without a structured plan, you risk:

Missing out on major tax deductions

Falling behind on long-term wealth

Depending solely on your business to fund your retirement

Feeling financially vulnerable later in life

Unlike employees who rely on employer-sponsored plans like 401(k)s, business owners have access to powerful, flexible, tax-advantaged retirement plans designed specifically for entrepreneurs, freelancers, and self-employed individuals.

Retirement planning is not optional—it’s part of building a stable, sustainable business.

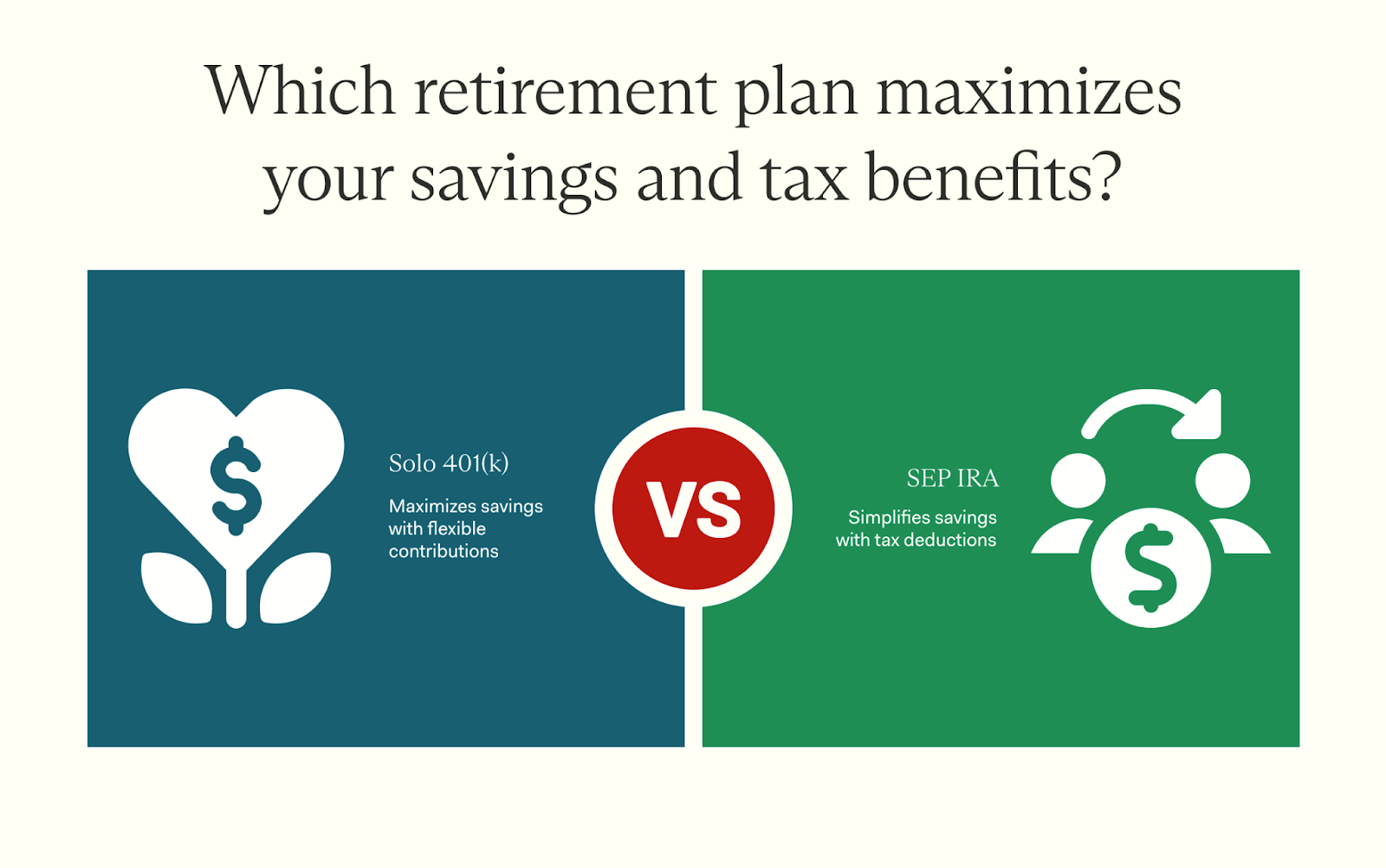

SEP IRA vs. Solo 401(k): Which Is Right for Your Business?

Both a SEP IRA and a Solo 401(k) offer generous retirement contribution limits and major tax benefits. The right choice depends on how your business is structured and how much you want to contribute.

⭐ SEP IRA (Simplified Employee Pension)

Best for:

✔ Solo business owners

✔ Businesses with employees

✔ Entrepreneurs wanting simple setup & low maintenance

Benefits:

Contribute up to 25% of your net earnings, up to IRS limits

Easy to administer

Tax-deductible employer contributions

No annual IRS filing requirement

Great option if you want something simple and flexible.⭐ Solo 401(k) (Individual 401(k))

Best for:

✔ Self-employed individuals with no employees

✔ High earners wanting to maximize contributions

✔ Business owners who want Roth options

Benefits:

Contribute as both the employer and the employee

Higher potential contribution limits

Option for Roth (after-tax) contributions

Allows loans, unlike a SEP IRA

This is ideal if you want to maximize contributions or need Roth flexibility.

Tax Advantages of Contributing Early and Consistently

One of the biggest benefits of retirement planning for small business owners is the tax savings.

How You Save on Taxes

Contributions are tax-deductible, reducing your taxable income

Investments grow tax-deferred (or tax-free with Roth)

Lower taxable income can help you qualify for additional deductions and credits

Starting early amplifies the benefits thanks to compound interest, turning small, consistent contributions into significant long-term wealth.

How Much Should You Really Be Saving?

There’s no one-size-fits-all number, but here’s a solid framework:

1. Aim for 15–25% of your income

Most financial planners recommend saving at least 15%, but business owners often target closer to 20–25% because income can vary.

2. Start with what feels manageable

Even $100/month creates momentum—and reduces the habit of relying fully on your business.

3. Increase contributions during strong months

Because your income fluctuates, take advantage of high-revenue months to contribute more.

4. Use a tax professional to calculate your exact allowable maximum

Especially with Solo 401(k)s and SEP IRAs, contribution rules can get tricky.

Integrating Retirement Planning Into Your Business Budget

Retirement planning becomes easy when it becomes a line item in your budget.

Here’s how to integrate it seamlessly:

Include retirement contributions in your monthly business expenses

Automate transfers so you don’t forget

Use profit-first style allocations to ensure consistency

Review contributions quarterly

Adjust as your business grows

Treat retirement contributions like payroll—not optional, not sporadic, but essential.

Mistakes That Can Cost You Big on Taxes and Growth

Avoid these common errors that hold small business owners back:

❌ Not having a retirement plan at all

You miss out on tax deductions and compound growth.

❌ Waiting until the end of the year

This often leads to rushed, smaller contributions.

❌ Mixing personal and business finances

Makes it harder to calculate accurate contributions and deductions.

❌ Failing to revisit your plan

Your retirement strategy should evolve as your income grows.

❌ Not getting professional guidance

This can lead to underfunding, overfunding, or missing tax breaks.

Leveraging Professional Advice for Maximum Benefit

Working with a financial professional or small business accountant can help you:

Choose the best retirement plan

Maximize tax deductions

Ensure compliant and optimized contributions

Balance retirement savings with cash flow

Strategically plan for long-term wealth

Business owners often leave thousands of dollars on the table—simply because they didn’t know what they were allowed to contribute.

Conclusion: Build Wealth Today, Enjoy Peace of Mind Tomorrow

Retirement planning isn’t just about money—it’s about confidence, stability, and long-term freedom.

As a small business owner, you have powerful tools at your disposal. With smart planning, consistent contributions, and tax-efficient strategies, you can create a future where:

✔ You’re not dependent on the business

✔ You’re financially secure

✔ You’re building generational wealth

✔ You can step back when you choose—not when you’re forced to

Book a consultation with us for more strategic assistance! https://calendly.com/kmtconsultingllc