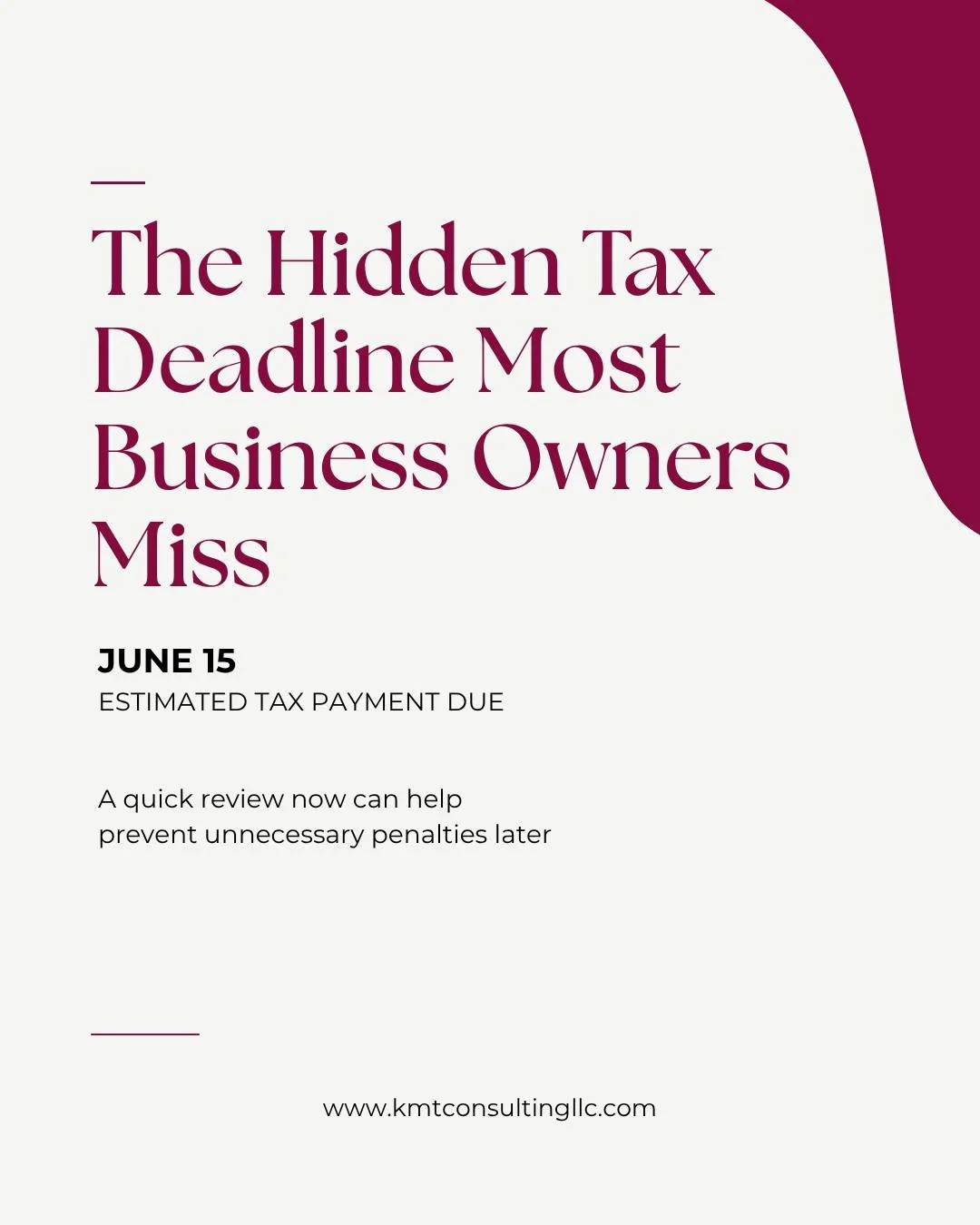

The Hidden Tax Deadline That Catches Small Business Owners Off Guard Every Year

Most business owners breathe a sigh of relief after April 15.

Tax returns are filed. Documents are submitted. The stress of tax season feels behind them.

But for many self-employed business owners, freelancers, and entrepreneurs, there's another important tax deadline just around the corner—and it's one that catches thousands of people off guard every year.

June 15.

Missing it can lead to penalties, interest, cash flow headaches, and an unpleasant surprise when tax season rolls around again.

Let's break down what this deadline is, who it affects, and how to stay ahead of it.

Why June 15 Matters More Than Most Business Owners Realize

Unlike W-2 employees, business owners typically don't have taxes automatically withheld from their income throughout the year.

Instead, the IRS requires many self-employed individuals to make estimated tax payments periodically.

The second estimated tax payment for 2026 is due on June 15.

The challenge?

Many business owners don't know this deadline exists.

Others know about it but aren't sure how much they should pay.

And some assume they'll simply settle everything when they file their tax return next year.

Unfortunately, the IRS doesn't work that way.

Taxes are generally expected to be paid as income is earned—not all at once after the year ends.

Who Needs to Make Estimated Tax Payments?

You may be required to make estimated tax payments if:

You own a small business

You're self-employed

You freelance or consult

You're a sole proprietor

You're a partner in a partnership

You're an S Corporation shareholder

You receive income that doesn't have taxes withheld

As a general rule, if you expect to owe at least $1,000 in taxes when you file your return, estimated tax payments are likely required.

If you're unsure whether this applies to you, that's often the first question worth asking before the deadline arrives.

The Mistake That Creates Penalties

One of the most common misconceptions among business owners is:

"I'll just pay everything when I file my return."

While that sounds reasonable, it can create unnecessary penalties and interest.

The IRS expects taxes to be paid throughout the year.

When payments are missed or significantly underpaid, penalties may be assessed—even if you ultimately pay your tax bill in full later.

The result?

You pay more than necessary simply because of timing.

The good news is that these penalties are often avoidable with proper planning.

The Q2 Quirk Most People Don't Know

Here's something many business owners don't realize:

The estimated tax calendar isn't divided into four equal quarters.

The June payment period covers income earned during April and May, making it shorter than many people expect.

This matters because business income often fluctuates.

If your revenue increased during the spring months, your estimated tax obligation may have increased as well.

Using outdated projections can lead to underpayments now and larger corrections later in the year.

That's why estimated taxes shouldn't be treated as a set-it-and-forget-it process.

They should evolve alongside your business.

How Much Should You Be Saving?

While every business is different, many owners use a simple starting guideline:

Set aside approximately 25%–30% of net profit for taxes.

However, your actual percentage depends on several factors, including:

Your business structure

State tax requirements

Household income

Deductions

Credits

Retirement contributions

This is where many business owners benefit from reviewing actual year-to-date numbers rather than relying on assumptions.

The more accurate your projections, the fewer surprises you'll face later.

How to Make Your Payment

If you determine that an estimated payment is due, the IRS offers several options:

IRS Direct Pay

A fast and secure option that allows you to pay directly from your bank account.

EFTPS (Electronic Federal Tax Payment System)

A popular option for business owners who prefer to schedule and track payments throughout the year.

Mail-In Payment

You may also submit payment using Form 1040-ES vouchers. Whichever method you choose, save your confirmation records and payment documentation. A few seconds of recordkeeping today can save significant frustration later.

The Difference Between Filing and Planning

Many business owners view taxes as something that happens once a year. Successful business owners view taxes as something they manage all year long. That's the difference between filing and planning. Filing tells you what has already happened. Planning helps you influence what happens next. When estimated taxes are reviewed regularly, you gain: Better cash flow visibility, more accurate tax projections, fewer surprises, greater confidence in financial decisions, and reduced risk of penalties. Most importantly, you stay in control instead of reacting when deadlines arrive.

Final Thoughts

The June 15 estimated tax deadline is one of the most commonly overlooked dates on the business owner's calendar. But it doesn't have to catch you off guard. Taking time now to review your income, tax projections, and savings can help you avoid unnecessary penalties and create a stronger financial foundation for the rest of the year.The goal isn't simply to stay compliant. It's to make informed decisions that support long-term business success.

Need Help?

At KMT Consulting, LLC, we help small business owners move beyond reactive tax filing and into proactive financial strategy. This includes calculating estimated payments, projecting year-end taxes, or building a tax plan that supports your growth goals. We're here to help. Don't wait until the deadline has passed. Visit www.kmtconsultingllc.com to schedule a consultation with us.